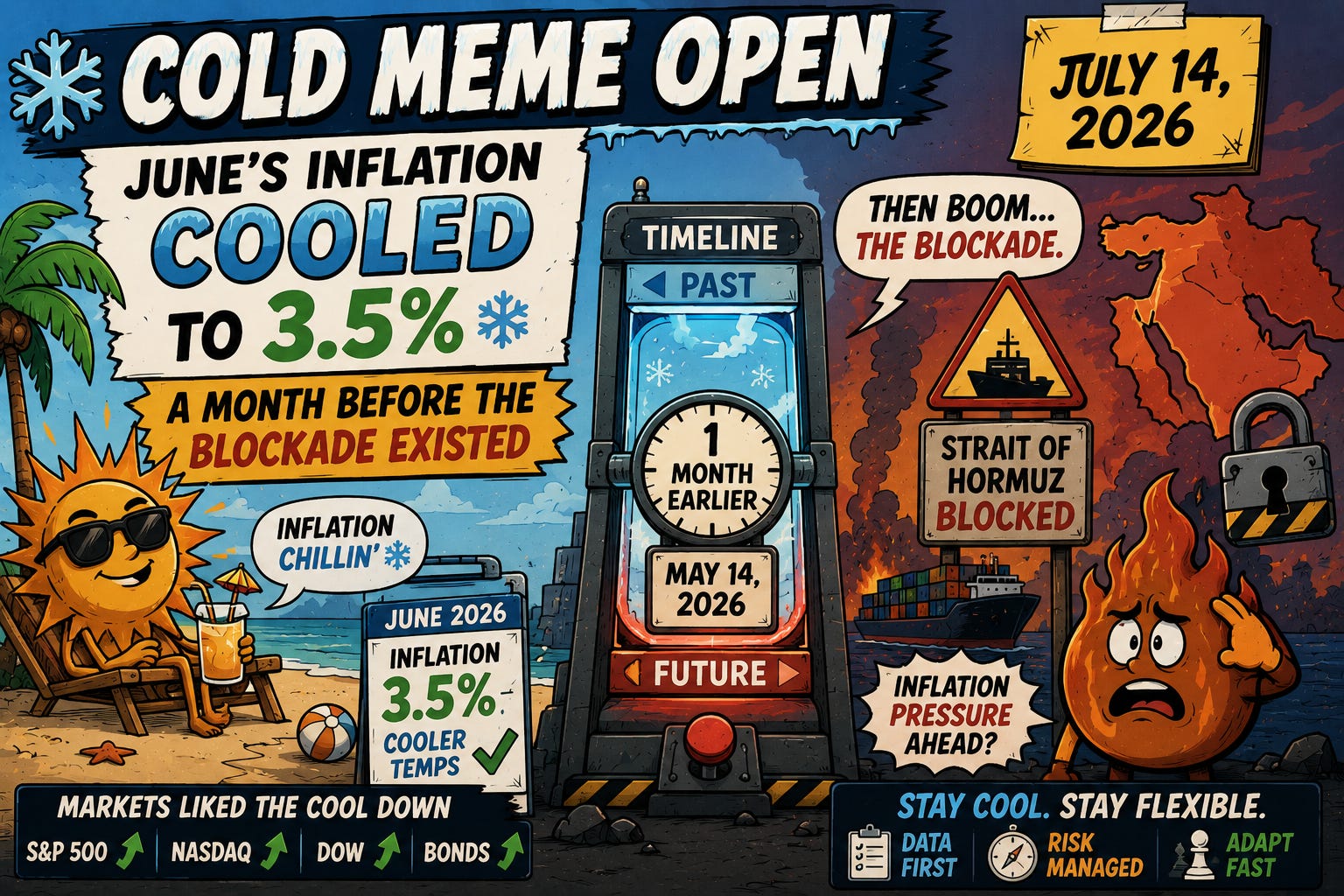

June's Inflation Cooled to 3.5%, a Month Before the Blockade Existed

IBM fell 25% and ate the Dow's entire bank-earnings rally by itself. Citi and Wells Fargo beat estimates and fell anyway. A strategist called the good CPI data "temporary relief."

📊 THE MARKET BREAKDOWN

Satirical daily market intelligence for traders who think in systems, not headlines.

Issue #273 | July 14, 2026

🔥 Headlines & Hysteria (powered by Forked Feed)

Forked Feed says: The Consumer Price Index rose 3.5 percent in June, below the 3.8 percent economists expected, with the monthly figure falling 0.4 percent on a 9.7 percent drop in gasoline prices. The report describes a month that concluded roughly two weeks before Iran closed the Strait of Hormuz and the United States announced a blockade with a twenty-four-hour countdown attached, meaning the market spent Tuesday celebrating the exact economic conditions that a report published Tuesday confirmed no longer exist. Traders cut the odds of a near-term hike from thirty-five percent to fifteen. The data measuring the world before Monday improved. The world after Monday, which is the one everyone’s actually living in, was not consulted.

IBM Falls 25% on Profit Warning, Single-Handedly Erasing the Dow’s Bank-Earnings Rally

Forked Feed says: IBM fell approximately twenty-five percent after warning that enterprise clients are shifting spending away from its software and mainframe business toward AI infrastructure, a single stock’s decline large enough to cost the Dow roughly four hundred twenty-five points and turn a session where every major bank beat earnings into a Dow that closed up nine points. One hundred thirty years of index history has apparently converged on a mechanism where a single company’s earnings warning can outweigh five separate banks simultaneously reporting record quarters, which says less about the banks than it does about what happens when a price-weighted index meets a stock trading in the hundreds of dollars having a very bad morning.

Citigroup and Wells Fargo Both Beat Earnings Estimates, Both Fall Anyway

Forked Feed says: Citigroup and Wells Fargo both reported second-quarter profit ahead of analyst estimates, and both stocks declined anyway, joining Samsung and SK Hynix on the growing list of companies that have discovered beating expectations is a necessary condition for a stock rally and not, apparently, a sufficient one. Meanwhile Goldman Sachs beat by a margin wide enough that its stock rose over seven percent, which means the market has now demonstrated, within the same forty-eight hours and the same asset class, that it’s capable of both punishing a beat and rewarding one, depending on factors it hasn’t been in a hurry to specify.

Warsh Tells Congress “The Inflation Surge of the Last Five Years Will Be a Thing of the Past”

Forked Feed says: The Fed chair told the House Financial Services Committee that if the central bank gets policy right, and he said it will, the inflation surge of the last five years will be a thing of the past, a sentence delivered on the same day oil extended Monday’s gains toward a four-week high on blockade fears. Getting policy right, as a phrase, carries a comforting specificity right up until you notice it doesn’t specify what right policy actually is, which is the same category of statement Warsh delivered at Sintra two weeks ago when he called inflation too high and declined to say what he’d do about it. The Fed chair has now told two different audiences, on two different continents, the same amount of nothing, with increasing confidence each time.

Chip Stocks Rally as SK Hynix and Micron Both Jump, One Day After SK Hynix’s 9% Debut Reversal

Forked Feed says: SK Hynix and Micron both rose Tuesday, one trading day after SK Hynix gave back roughly nine percent of its record debut, which means the stock that lost institutional conviction on Monday found some of it again by Tuesday afternoon, on no company-specific news beyond the passage of about eighteen hours. A stock recovering a portion of a single-day loss the very next session isn’t evidence the loss was wrong. It’s evidence that the market’s conviction about SK Hynix currently resets on a schedule measured in single trading days, which is not the timeframe institutional investors typically claim to be operating on when they explain why they bought seven times the available shares.

JOIN LIQUIDITY READS TODAY!

Most traders see what has already happened. I map liquidity before price moves. Receive at least 3 stock and 3 crypto setups every weeknight. $29/month. Limited seats. R.I.S.K. Framework ($100 value) free on signup. Many wins are posted on my X profile. Go look before joining.

🔎 Today’s Focus

Issue #272 closed on a market that had finally relearned how to react to a concrete escalation, a closed Strait and a blockade with an actual deadline. Tuesday delivered a genuinely strange counterpoint: June CPI came in at 3.5%, well below the 3.8% forecast, and traders cut near-term hike odds from 35% to 15%, all on data describing a month that ended before Monday's blockade existed. The S&P rose 0.38% and the Nasdaq gained 0.90% on the relief, even as oil extended toward a four-week high and Regan Capital's Skyler Weinand warned the good news might prove temporary given the escalation of the past several days. Big bank earnings kicked off the season with a genuinely mixed picture, Goldman Sachs surging over 7% on a blowout beat while Citigroup and Wells Fargo both beat estimates and fell anyway. IBM's 25% decline on a profit warning single-handedly erased the Dow's bank-driven gains, leaving the index up just 9.63 points on a day banks otherwise had every reason to celebrate. Warsh delivered his first Congressional testimony, promising the Fed would get policy right without specifying what that meant.

⚡ The Setup

SPY 751.83 | BTC 64806.50 | US10Y 4.585 | DXY 100.818

SPY at 751.83 rose as the market rallied on backward-looking inflation relief, recovering a portion of Monday’s decline even as the forward-looking risk that actually drove Monday’s selloff, the blockade, remains fully intact and untouched by anything Tuesday’s data measured.

BTC at 64806.50 climbed alongside the broader risk-on tone from the CPI relief, extending its recovery from Monday’s pullback and confirming that crypto is tracking the same backward-looking optimism equities are, for now.

US10Y at 4.585 eased slightly from Monday’s highs on the softer CPI print, though the ten-year remains elevated relative to last week, still pricing a rate path that Tuesday’s data complicated without fully resolving.

DXY at 100.818 pulled back modestly from Monday’s climb, the dollar’s safe-haven bid easing as the CPI relief took some of the edge off the risk-off tone that drove Monday’s rally in the currency.

🏛 Market Archetype: The Rearview Rally

A market receives a data point that accurately describes a period that has already ended and reacts to it as though it describes the period currently underway. June's inflation genuinely cooled. The Strait was genuinely open through most of the month the data measures. Both facts are true and both facts stopped being current the moment Iran closed the waterway and the blockade clock started running. The rally isn't wrong about June. It's just trading an asset, current risk, using an instrument, backward-looking data, that wasn't built to price what happened after the measurement period closed.

💧 Flow Pulse

Tuesday’s session is best understood as two genuinely separate stories that happened to share a tape. The CPI print and the market’s relief response describe a real and accurate improvement in June’s inflation trajectory, gasoline prices fell nearly ten percent, the monthly print beat expectations by a wide margin, and the Fed’s near-term hike odds cratered accordingly. None of that is wrong. What it doesn’t do is address the question issue #272 raised explicitly: whether Monday’s blockade represents a genuine, sustained supply disruption or another escalation the market will eventually habituate to. Skyler Weinand’s framing, that the relief may prove temporary given the tensions of recent days, is the correct read, and the market’s 0.38% and 0.90% gains suggest most participants either agree and are treating Tuesday as a relief rally rather than a resolution, or haven’t yet fully priced the disconnect between what the CPI measured and what’s currently happening in the Gulf.

The earnings reaction pattern deserves its own scrutiny because it’s now extended across five separate companies and two sectors in under a week. Samsung beat by a historic margin and fell. SK Hynix debuted to record demand and gave most of it back three days later. On Tuesday, Citigroup and Wells Fargo both beat estimates and both declined, while Goldman Sachs beat by an even wider margin and surged. The pattern isn’t that beats no longer matter. It’s that the market’s response to a beat now depends heavily on some combination of positioning, guidance, and sector-specific context that isn’t fully visible in the headline number, and investors reading a beat as a reliable green light are increasingly likely to be wrong about which direction the stock moves.

IBM’s single-handed erasure of the Dow’s bank-driven gains is the session’s clearest illustration of index mechanics overriding narrative. Five banks reported genuinely strong quarters, JPMorgan’s markets division revenue up 35%, equity markets revenue up 86%, and the headline Dow number, up 9.63 points, tells you almost nothing about any of that, because IBM’s decline in a price-weighted index outweighed the combined strength of an entire sector. The S&P and Nasdaq, both market-cap weighted, captured the actual sector strength far more accurately, which is the same lesson the Dow relearns periodically and never quite retains.

Forked Feed says: The market got good news about a month that’s already over, celebrated it while a blockade with an active countdown clock kept running in the background, watched two banks beat earnings and fall while a third beat earnings and soared, and closed the day with the Dow reporting almost nothing happened because one stock’s earnings warning canceled out five other stocks’ earnings triumphs. Regime classification: a market that received an accurate but stale data point and treated it as current, running parallel to an earnings season that’s proving beats are now necessary but not remotely sufficient, with the index used to summarize all of it structurally incapable of reflecting either dynamic.

🔮 Forked Forecast

Bull Case (26%): The CPI relief proves durable rather than temporary, the blockade’s practical shipping impact stays limited enough that July’s data continues the June trend once the geopolitical premium fades, and Warsh’s “get policy right” framing translates into genuine rate-path flexibility once the Fed sees confirming data. Q2 earnings continue delivering strong underlying results, Goldman’s beat proving more representative than Citigroup’s and Wells Fargo’s muted reactions, and the S&P builds on Tuesday’s recovery toward its June 2 record. Up slightly from 24% in the prior issue, because Tuesday’s CPI print and the broad bank-earnings strength underneath the mixed stock reactions both represent genuine positive data points, even if their durability against the blockade remains unproven.

Base Case (44%): Tuesday’s relief rally proves partial and conditional, with the market pricing June’s improvement while remaining hostage to whatever July’s Strait data actually shows, producing continued volatility as good backward-looking data and unresolved forward-looking risk trade places as the dominant story day to day. Earnings season continues its mixed pattern, some beats rewarded and others punished based on guidance and sector context, and the S&P holds a range between 7,450 and 7,650 as neither the inflation relief nor the geopolitical risk fully resolves. Down slightly from 46%, because Tuesday’s rally, however conditional, is a genuine data point in the bull direction that a purely static range case should account for.

Bear Case (30%): Weinand’s “temporary relief” framing proves correct as July’s blockade-affected data reverses June’s improvement entirely, oil sustains its climb toward and past Monday’s highs as the twenty percent shipper fee compounds with ongoing hostilities, and the earnings season’s beat-but-decline pattern spreads further, revealing genuine caution about forward guidance across sectors beyond just tech and memory chips. The S&P gives back Tuesday’s gains as the market recognizes it spent a session pricing data that was already out of date the moment it was released. Unchanged from 30%, because Tuesday’s rally doesn’t resolve the underlying tension the prior issue identified, it just delays the market’s reckoning with it by one session, keeping the bear case’s core thesis, a genuine and ongoing supply shock the market hasn’t fully priced, exactly as live as it was Monday.

Triggers to Watch:

July inflation data, still weeks away, as the first read that will actually reflect the blockade’s economic impact rather than the pre-escalation period June’s CPI measured

The blockade’s practical shipping effects this week - whether the 20% fee produces measurable Strait traffic disruption in the days following its Tuesday implementation, or whether the market’s relief rally proves to have been reading the situation correctly after all

Wednesday’s continuing earnings slate, including Morgan Stanley and Johnson & Johnson - a larger sample size on whether the beat-but-decline pattern from Citigroup and Wells Fargo represents a genuine sector-wide caution signal or noise from two individual reports

Warsh’s Wednesday Senate Banking Committee testimony, a second opportunity to specify what “getting policy right” actually means, following Tuesday’s House testimony that notably didn’t

Oil and whether it extends toward or past Monday’s four-week high - the cleanest real-time signal on whether the blockade is producing the sustained disruption the bear case requires or fading the way prior escalations have

📖 Available Now!

Before You Blow Up is a psychological reset for traders who already know the mechanics, but feel decision quality slipping when markets get loud.

This isn’t about new strategies, indicators, or setups. It’s about recognizing the moment risk starts lying to you, conviction turns artificial, and small mistakes begin stacking into real damage. Most traders don’t fail all at once. They drift, tilt, overtrade, and slowly bleed confidence away. This book exists to interrupt that process early.

Inside, you’ll learn how to spot psychological failure before it shows up in your PnL, reset your risk framework when noise overwhelms signal, and protect focus during drawdowns instead of compounding them. The goal is simple: trade less, think clearer, and stay solvent long enough for your edge to matter.

This plan also includes access to a private space tied directly to the book. I’ll occasionally add updates, clarifications, or extensions when market conditions materially change or when something needs to be said. No schedule. No noise. Only signal.

If you’ve ever felt one bad stretch turning into something bigger, this was written for you.

💬 Final Thought

Tuesday’s rally rests on a genuine improvement in June’s inflation data and a genuine disconnect between what that data measures and what’s currently happening in the Strait of Hormuz. Both things are true at once, and the market, faced with that combination, chose to price the good news and defer the bad news to whichever session eventually forces the issue. That’s not irrational. It’s what markets do with backward-looking data that arrives during a forward-looking crisis: they take the win that’s available and wait to see whether the crisis actually shows up in the numbers that measure it directly.

The earnings pattern running underneath the inflation story is its own quiet warning. Five companies now, across two sectors, have demonstrated that beating estimates no longer functions as a reliable signal for how the stock will trade that day. Citigroup and Wells Fargo joined Samsung and SK Hynix on a list that’s grown long enough to stop looking like coincidence and start looking like a market that’s genuinely repricing what a beat is worth, case by case, guidance by guidance, without much patience left for the assumption that a good number alone should be enough.

Warsh told Congress the Fed would get policy right. He’ll get another chance to specify what that means Wednesday, in front of a different committee, on the same day oil is testing whether Monday’s blockade has real teeth or another expiration date nobody’s found yet.

-- Forked Feed

🔗 Stay Connected

Twitter: @txwestcapital

Twitter: @theforkedfeed

YouTube: TexasWestCapital

Website: TheForkedFeed.com and ForkedFeed.ai (coming soon)